Tax laws changes affecting payroll, 2022

12 Dec 2021TAX LAWS CHANGES AFFECTING PAYROLL AS OF JANUARY 1, 2022

Minimum monthly salary (MMA) rises to 730 EUR

We would like to inform that as of 1st of January 2022 minimal salary rises from 642 EUR to 730 EUR and the minimal hourly wage – from 3,93 EUR to 4,47 EUR.

This amendment is applied automatically to employees who receive minimum salary or salary lower than 730 EUR (or respectively lower than hourly rate of 4,47 EUR). Minimum monthly / hourly wage increase will affect the mentioned above employees’ vacation, sick leave pay or any other pay that is calculated with average during the period of January to March, 2022. This decision will set that per diem pay for trips abroad are tax exempt when employee salary is higher than 1204,50 EUR (before was 1059,30 EUR) or hourly payment is higher than 7,38 EUR / h (7,3755 EUR / h).

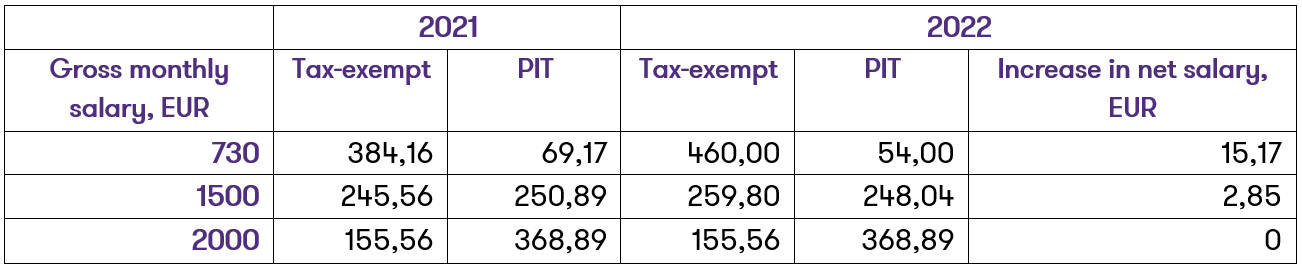

Changes in the tax-exempt amount of income (NPD)

Personal income tax (further – PIT) law amendments change calculation of nontaxable income from 1st of January, 2022 - two formulas will be used to calculate tax-exempt amount, also fixed tax-exempt values will be altered.

1) When salary is less than minimum salary as of January 1 (year 2022 – 730 EUR) – fixed monthly nontaxable amount of 460 EUR to be used (previously 400 EUR);

2) When salary is between minimum salary as of January 1 (year 2022 – 730 EUR) and 1678 EUR the formula shall be:

Monthly nontaxable income = 460 – 0,26 x (earned monthly salary - minimum monthly salary).

3) When salary exceeds EUR 1 678, the following formula shall be:

Monthly nontaxable income = 400 – 0,18 × (earned monthly salary – 642).

Considering the changes of tax-exempt formula, the table below shows few examples:

For persons with 0-25 percent incapacity to work, or are of retirement age with high level of special needs, and severely disadvantaged persons the monthly nontaxable amount increasing from 645 EUR to 740 EUR. Fpr persons with 30-55 percent incapacity to work, or are of retirement age with a moderate level of special needs and persons with mild disability – the monthly nontaxable amount is increasing from 600 EUR to 690 EUR.

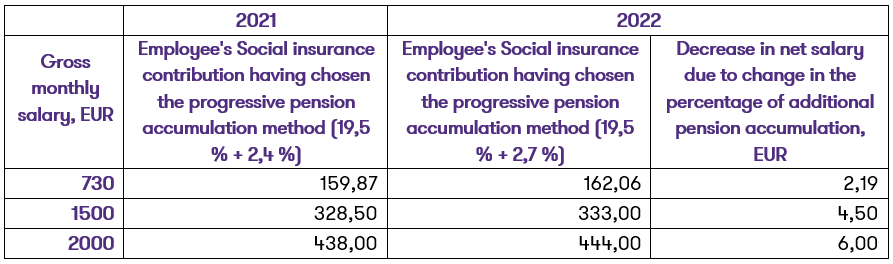

Social insurance rate change for participants in Pensions savings scheme

Participants in Pensions savings scheme contribution rate increases from 2,4% to 2,7%. No changes for those whose rate already was 3%.

Below you can find example calculations of employee social security contributions from earnings using the progressive pension method: