Subscribe to audit, accounting, tax, legal and business consulting news. Be the first to receive Grant Thornton Baltic news, expert advice, professional business insights and event information.

Tax laws changes affecting payroll as of January 1, 2024

Tax laws changes affecting payroll as of January 1, 2024

Minimum monthly salary (MMA) rises to 924 EUR

The 28th of June 2023 Government of the Republic of Lithuania ruling No. 516 "Regarding the Minimum Wage Applicable in 2024” comes into force as of 1st of January 2024 where minimal salary rises by 84 EUR – from 840 EUR to 924 EUR and the hourly wage – from 5,14 EUR to 5,65 EUR.

This amendment is applied automatically to employees who receive minimum salary or salary lower than 924 EUR (or respectively lower than hourly rate of 5,65 EUR). Minimum monthly / hourly wage increase will affect the mentioned above employees’ vacation, sick leave pay or any other pay that is calculated with average during the period of January to March, 2024. This decision together with decision below about business trips also will set that per diem pay for trips abroad are tax exempt when employee salary is higher than 1524,60 EUR (before was 1386 Eur) or hourly payment is higher than 9,32 EUR / h (9,3225 Eur / h).

Changes in the tax-exempt amount of income (NPD)

Also there are changes in Personal income tax (further – PIT) law articles IX-1007 amendments from which the most relevant to payroll is Article 20. It relates to changes of nontaxable income: the formula used to calculate the tax-exempt amount will be changed since 1st of January, 2024 (two formulas will be used) and other fixed tax-exempt values will be altered.

The nontaxable income for the tax period is subject to the following procedure:

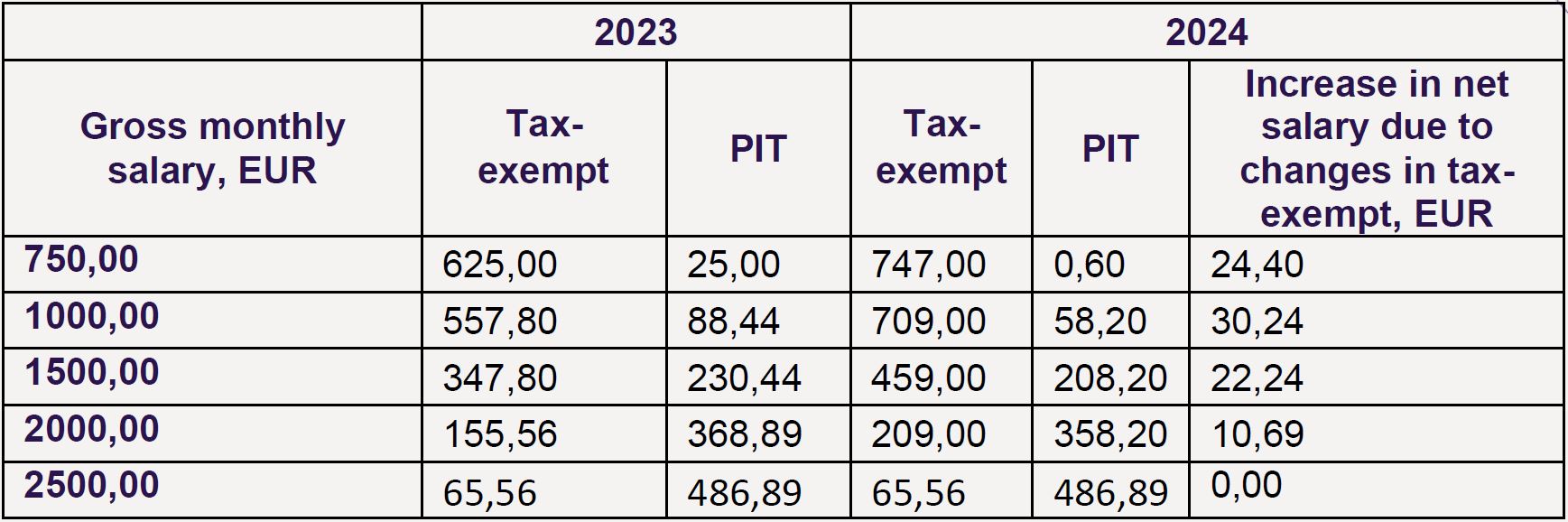

1) a person whose monthly income does not exceed the minimum monthly salary valid for current calendar year applies for a monthly nontaxable amount of 747 EUR (previously 625 EUR);

2) for a person whose monthly income related to an employment relationship or alike exceeds the minimum monthly salary valid for current calendar year, however, does not exceed 2 167 EUR, the following formula is applicable:

3) for a person whose monthly income related to an employment relationship or alike exceeds EUR 2 167 EUR, the following formula is applicable:

| Monthly nontaxable income = 747 – 0,5 x (earned monthly income related to employment relationship – minimum monthly salary applicable for the calendar year). |

3) for a person whose monthly income related to an employment relationship or alike exceeds EUR 2 167 EUR, the following formula is applicable:

| Monthly nontaxable income = 400- 0,18 × (earned monthly income related to employment relationship 642). |

Considering the changes of tax-exempt formula, the table below shows PIT calculations from sample salary sums:

For persons who have been assigned 0-25 percent incapacity for work, or persons who have reached the retirement age, have a high level of special needs according to the procedure established by law, or persons who are severely disadvantaged under the statutory procedure, the monthly nontaxable amount is 1 127 EUR. Persons who have been assigned 30-55 percent incapacity to work or persons who have reached the retirement age, who have a moderate level of special needs in accordance with the procedure established by law or mild disability levels – the monthly nontaxable amount is 1 057 EUR.

Authors

-

Inesa Greičė

Inesa Greičė - Grant Thornton Baltic UAB Partner | Head of Payroll DepartmentView Profile

Subscribe to our newsletter