Lithuania 2026 tax reform. Overview of initial drafts.

DEFENSE FUND FINANCING INCREASE

Defense fund financing sources (from 2026)

It is expected that the Defense Fund will additionally consist of:

- 2% of personal income tax directly allocated to the fund;

- State revenue from the newly introduced security contribution, calculated from non-life and property insurance premiums;

- 50% of non-commercial real estate tax and the entire additional 0.2% real estate tax for commercial real estate.

In addition, it is intended to allocate a larger share of budget revenues to the Defense Fund, received from:

- Corporate income tax (CIT) - from 1.9% in 2025, to 8% in 2026 and 11.2% from 2027;

- Excise duties - from 4.1% in 2025, to 8% in 2026 and 8.4% from 2027.

These changes are based on the geopolitical situation and the need to ensure long-term stability in defense financing, especially in response to regional threats and strengthening NATO commitments.

New security contribution (from non-life insurance agreements)

A new mandatory security contribution is proposed for national security financing:

- 10% of non-life insurance premiums (e.g., property, travel insurance);

- 0% rate for mandatory civil liability insurance contracted with individuals.

The contribution will supplement Defense Fund revenue and be administered through insurance companies.

PROPOSED CORPORATE INCOME TAX CHANGES

Rate increase by 1 percentage point

A standard corporate tax rate increase from 16% to 17% would take effect in 2026. This would also increase the rate for small businesses from 6% to 7%.

Small business tax relief (0%) extended from 1 to 2 years

The period during which newly registered small businesses will be subject to a 0% corporate tax rate on profits earned is being extended. This period will be extended from 1 to 2 years in order to provide additional support to growing businesses.

New "Instant" depreciation allowance for fixed assets

It is envisaged to allow a possibility of applying instantaneous depreciation of fixed assets to the asset groups "Machinery and equipment", "Equipment (structures, wells, etc.)", "Computer equipment and communications equipment", "Software", "Acquired rights", and "Trucks, trailers and semi-trailers".

This preferential instantaneous depreciation does not apply to assets that are subject to the investment projects relief under Article 46-1 of the Corporate Income Tax Law (i.e., it is possible to chose, to either depreciate immediately but only once through instantaneous depreciation, or twice - by applying the investment projects relief and then also further depreciating the asset in the "classic" way).

Restriction on group loss carryforwards

It is planned to limit the possibility of tax loss carryforwards to 70% of the company's taxable income. It is also determined that the conditions of duration (2 years) and scope (2/3) of group membership are assessed on the last day of the period, and not at the moment of transfer, as previously established by the Supreme Administrative Court of Lithuania. The motivation is indicated as the desire to prevent abuses.

STEM Scholarship Deduction

A possibility is envisaged for companies to deduct scholarships for students and researchers in the STEM fields (science, technology, engineering and mathematics) as expenses, up to EUR 2,500 per tax period under tripartite agreements, in order to promote science and technology.

PROPOSED CHANGES TO THE PERSONAL INCOME TAX

Personal Income Tax (PIT)

It is planned to change the PIT rates, applying them taking into account the total annual amount of all types of income, except income from distributed profits:

- The portion of income not exceeding 36 average salaries (~75,920 EUR) would be taxed at a rate of 20%;

- The portion of income exceeding 36 average salaries (~75,920 EUR) but not exceeding 60 average salaries (126,533 EUR) would be taxed at a rate of 25%;

- The portion of income exceeding 60 average salaries (~126,533 EUR) but not exceeding 120 average salaries (253,066 EUR) would be taxed at a rate of 32%;

- The portion of income exceeding 120 average salaries (~253,066 EUR) would be taxed at a rate of 36%. However, on April 23, the ruling party's speeches indicate that this rate is likely to be abandoned as too high, leaving the maximum rate at 32%. Therefore, the draft laws are still in the process and may change.

Individual business income would be taxed at a rate of 20%, but “credits” are possible. For example, for income not exceeding 20 thousand EUR, the effective rate after the credit becomes ~5%.

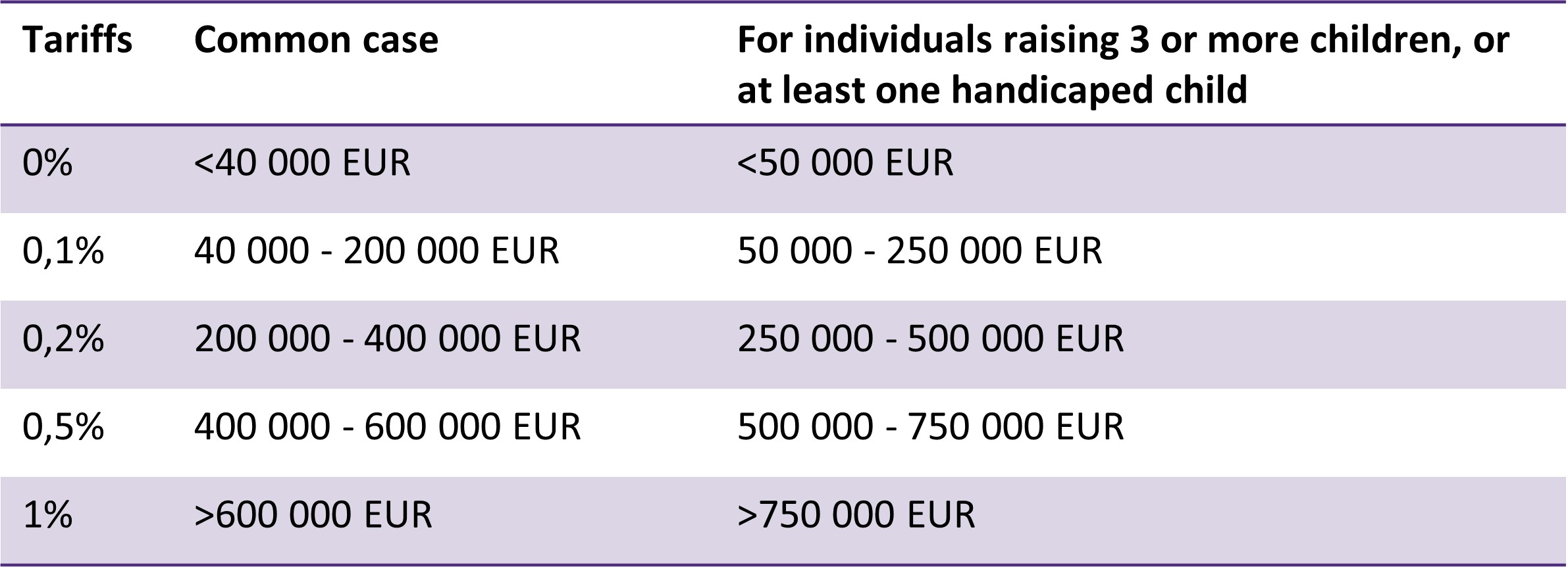

PROPOSED CHANGES TO REAL ESTATE TAX

Real Estate Tax

- An additional 0.2% tariff component has been established for commercial real estate (to the state budget / defence fund);

- Real estate valuation to determine the tax value will be carried out at least every 3 years (now – 5 years);

- 50% relief for housing declared as a place of residence (for the part of the real estate value up to 450 thousand EUR).

- 75% relief for housing declared as a place of residence for families with 3 children or raising a disabled child (for the part of the real estate value up to 450 thousand EUR);

- It is proposed to exempt persons entitled to receive compensation for housing heating costs.

*Example: With a property value of 199,999 EUR, the annual tax would be ~ 200 EUR, and if a place of residence is declared in that real estate, living alone - 100 EUR, two co-owners - 50 EUR.

PROPOSED VAT AND EXCISE DUTIES CHANGES

VAT Changes

The reduced VAT rate will be increased to 12% (from 9%) for:

- Accommodation services;

- Passenger transport services;

- Attendance at art and cultural events and institutions.

The reduced VAT rate will be decreased to 5% (from 9%) for:

- Books and non-periodical informational publications.

The 9% rate for heating, firewood, and hot water will be abolished - the standard 21% rate will be applied.

Excise duties changes

In order to contribute to the financing of state defense and public health policy goals, it is proposed to tax non-alcoholic sweetened beverages, energy drinks, and beverage concentrates, thus avoiding a potential substitution effect.

-

Vykintas Valiulis Vykintas Valiulis is Tax Partner at Grant Thornton Baltic UAB. He has more than 15 years of experience in the field of taxation, 6 of them he worked in one of the Big 4 audit and business consulting companies where Vykintas has gained significant experience in consulting the largest Lithuanian and foreign companies on tax issues.

Vykintas Valiulis Vykintas Valiulis is Tax Partner at Grant Thornton Baltic UAB. He has more than 15 years of experience in the field of taxation, 6 of them he worked in one of the Big 4 audit and business consulting companies where Vykintas has gained significant experience in consulting the largest Lithuanian and foreign companies on tax issues.View Profile