Subscribe to audit, accounting, tax, legal and business consulting news. Be the first to receive Grant Thornton Baltic news, expert advice, professional business insights and event information.

On 20 of March 2023 Ministry of Finance of Lithuania revealed proposals on tax reform, to be submitted to Parliament early May, to enter into force from the year 2024 (if adopted). Below we summarize key aspects of the tax reform, relevant for the businesses.

Contents

Corporate Income Tax – proposed key changes from 2024

- Instant fixed assets depreciation (fully in the first year of use), for machinery, computer equipment, software, acquired rights, cargo vehicles (incl. not new assets and assets purchased until 2024). However, it will not be applicable to those assets to which investment projects relief is applicable.

- Keeping unchanged R&D and “patent box” tax reliefs, as well as prolonging until 2028:

- investment projects relief;

- film funding relief.

- Lower tax burden for a wider range of small companies:

- Reduced 5% corporate income tax rate will be applicable to companies of up to 300k EUR turnover (incl. with related companies) but disregarding their headcount (previous 10 employee limit to be abolished).

- Exemption from advance payment of corporate income tax for companies with up to 500k EUR turnover (currently - 300k EUR).

- Abolishing sectorial tax reliefs:

- Life insurance companies – part of the insurance premiums, which can be considered as compensation for provided services, will be included into taxable base (but also allowing related deductions).

- Health care companies – income for services financed from public health insurance fund will be included into taxable base (but also allowing related deductions).

- Other changes in corporate income tax:

- Relief for risk and private capital subjects (RPCS) will be denied to structures where investments are made into companies related with RPCS shareholders.

- Company car expenses will be allowed depending on their CO2 emissions:

- Car purchase expenses deduction limits:

- 75k EUR, if CO2 is 0g/km

- 50k EUR, if CO2 is <130g/km

- 25k EUR, if CO2 is >130g/km, but <200g/km

- 10k EUR, if CO2 is >200g/km

- Car rent expenses deduction limits will be proportional to the above purchase limits divided by depreciation norm (which in most cases will be 6 years). E.g., for a company car of 100g CO2 emission, yearly rent expenses of up to 8,333 will be deductible (50,000 EUR / 6 years).

- Car usage and repair expenses deduction will be allowed proportionally to deductible purchase or rent expenses divided by actual cost of car. E.g. if actual car cost is 60k EUR, but due to 100g CO2 emission only 50k EUR can be deducted (83%), then only 83% of usage and repair costs will be deductible.

- Car purchase expenses deduction limits:

- Goodwill amortization for tax purposes will be denied if goodwill results from transaction between related parties or if acquiring entity is merged into the acquired entity. However, merging of acquired entity into the acquiring entity will be allowed. In addition, goodwill amortization period is shortened from 15 to 10 years.

- Transfer of tax losses between group companies will be limited to up to 70% of taxable profit of the receiving entity.

Personal Income Tax – proposed key changes from 2024

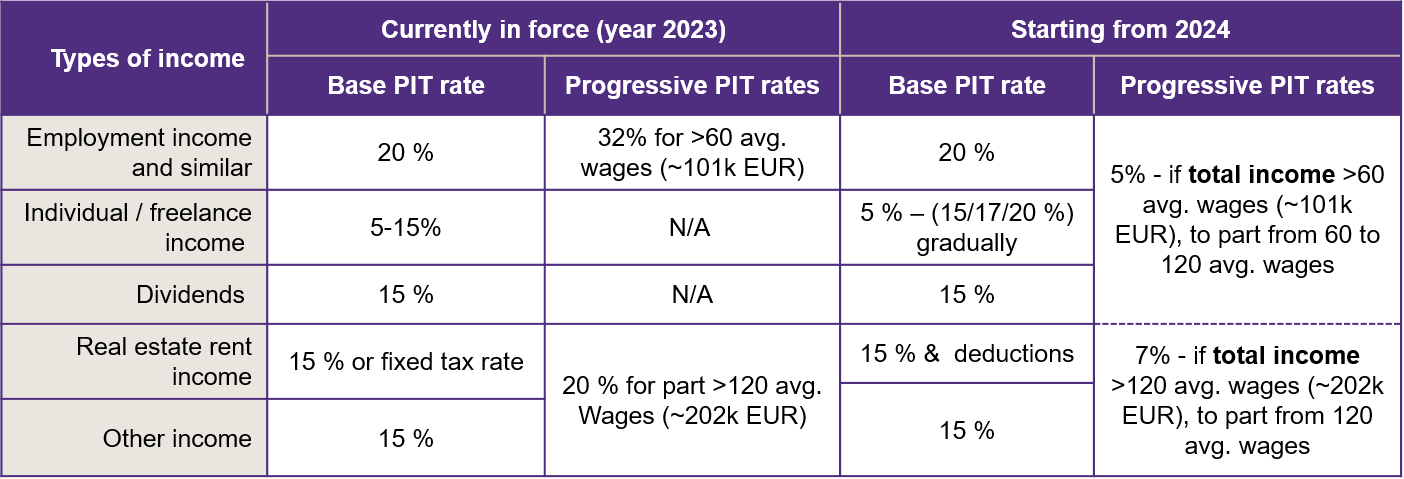

- Changes in progressive Personal Income Tax (PIT) mechanism from 2024:

- Abolishing of the 32% rate as currently in force (which were applied separately to labour income and to other types of income).

- Setting new additional progressive tax rates, to be applied if total income exceeds thresholds:

- Additional +5% PIT rate for total yearly income exceeding 60 average salaries (~101k EUR).

- Additional +7% PIT rate for total yearly income exceeding 120 average salaries (~202k EUR).

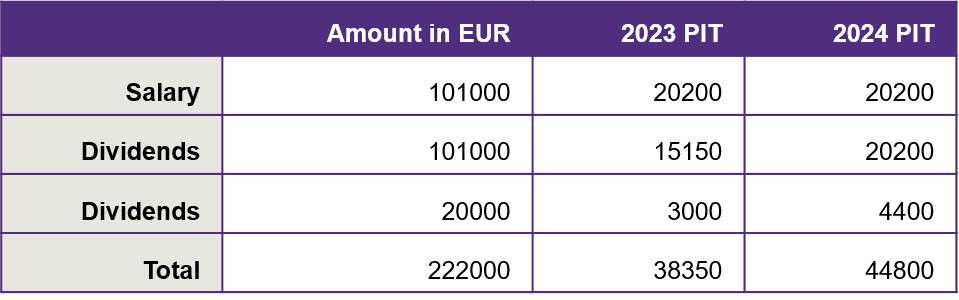

Example No. 1: if individual’s total yearly income is 222k EUR, from which 101k EUR from employment, and the remaining 121k EUR from dividend, then dividend revenue from 101k to 202k EUR will be taxed with 20% PIT rate (15% base tax rate + 5% additional progressive tax rate), and remaining 20k EUR dividend will be taxed with 22% PIT rate (15% base tax rate + 7% additional progressive tax rate). In such case individual’s total tax burden in year 2024 will be higher than in the year 2023.

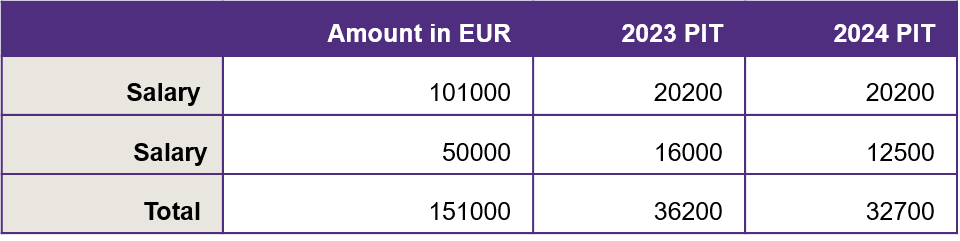

Example No. 2: if highly skilled individual’s total yearly income is employment only (salary, incl. bonuses) and reaches 151k EUR, then salary up to 101k EUR will be taxed the very same way as in year 2023, but the exceeding 50k EUR will be taxed not with 32% PIT rate as currently, but only with 25% PIT rate. In such case individual’s total tax burden in year 2024 will be lower than in the year 2023.

More details are shown in table below (source – Ministry of Finance)

- Individual activities personal income tax is set to gradually increase base and make taxation very close to employment relations:

- In 2024 – to increase taxable base by reducing automatic deductions from 30% to 20% and disallowing deduction of social and health security contributions. If VAT registration threshold is exceeded – prohibit automatic deductions and allow only those supported by expense documents.

- In 2025 – to increase base PIT rate from 15 to 17%.

- In 2026 – to increase base PIT rate for individual activity from 17 to 20% (as in employment).

- N.B. - this is by far the most controversial proposal in the tax reform package and thus not very likely to be adopted by Parliament without major amendments.

- A neutral “Investment account” instrument from 2024:

- Make it possible for the resident to choose an account and declare as investment account

- Return on investment (profit) obtained through Investment account will be taxed only if not reinvested. However, reinvestment is required during the same year when the income was received, which may be problematic for income received during the very last days of calendar year.

- Maximum non-taxable acquisition value of investments under the Investment account instrument is set to 10.000 Eur only but excludes costs of instruments purchased from the gains received from the Investment account.

- Losses from the Investment account will be allowed to be carried forward to the next year.

- Investment account can be held in financial institutions outside of Lithuania, in countries belonging to the European Economic Area (EU+EFTA), OECD (incl. U.S.A., Canada), or any other country with which Lithuania has a Double taxation avoidance treaty.

- Prohibition of deductions from Personal income tax base for payments made under new agreements of:

- Long-term life insurance

- III pillar pension.

- Stock options relief prolongation till after the end of employment contract. However, maintaining employment relations for at least 3 years’ condition remains (thus will not apply to “bad leavers”).

Other proposed tax reform elements

- VAT registration threshold will be increased from 45 to 55k EUR

- Changes of Real estate tax for individuals – however it is minor as average tax will be about 14 Eur/year

- Energy products taxation with excises according to pollution level

Ending remarks: to enter into force from 2024, all the above proposals will have to be debated and approved by Parliament until end of June 2023.

Please contact your tax advisors to learn more in detail how the proposed changes may affect your business.

Authors

-

Inesa Greičė

Inesa Greičė - Grant Thornton Baltic UAB Partner | Head of Payroll DepartmentView Profile

Subscribe to our newsletter