Changes in the Lithuanian legislation in 2018

23 Jan 2018As 2018 has begun, we would like to draw your attention to the latest important changes in the Lithuanian tax legislation. At the end of 2017 the Parliament passed changes to the laws on Personal income (LPIT) and Corporate income (LCIT) taxes.

Main changes in LPIT:

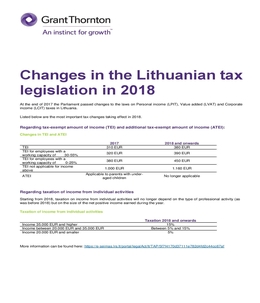

Regarding tax-exempt amount of income (TEI) and additional tax-exempt amount of income (ATEI):

- Starting from 2018, the TEI will be increased from 310 EUR to 380 EUR. Regarding the TEI for the disabled, people with a working capacity of 30-55 % and 0-25 % will be eligible to TEI of 390 EUR and 450 EUR accordingly. The TEI will lose its effect for incomes higher than 1160 EUR (before taxes), because of this, even the average income earning individuals will notice a positive effect.

- ATEI starting from 2018 will no longer be applicable.

Regarding income from individual activities:

The Parliament has agreed to the changes on LPIT according to which the taxation on income from individual activities, starting from 2018, will no longer depend on the type of professional activity (as was before 2018) but on the size of the net positive income earned during the year.

A standard tax rate of 15% will be applicable to all persons engaging in individual activities. In practice the 15% tax rate will only apply to annual positive incomes above 35 thousand EUR. Positive incomes that are smaller than 35 thousand EUR will have a gradually smaller tax rate, decreasing along with the smaller positive incomes (same principle as with TEI). The minimal Personal income tax rate on net positive incomes from individual activities will be set at 5% for positive incomes equal or smaller than 20 thousand EUR.

More information in Lithuanian can be found here.

Main changes in LCIT:

- The tax relief for investments into fixed assets will be continued – for the period starting from 2018 up to 2023 the taxable income can be reduced by up to 100% (previously up to 50%);

- Capital gains from the sale of subsidiary shares will be tax exempt if prior to the transaction at least 10% of the company shares were held for 2 years (previously holding at least 25% of shares was required);

- The rules on representation cost deductibility are changed:

- not more than 50% of costs incurred from representational activities can be deducted from the taxable income AND;

- the deducted amount cannot be larger than 2% of the revenue for the tax period. (Costs incurred from betting or gambling are not regarded as representational).

- The profits generated from the commercialization of inventions (scientific research and experimental development) will be taxed at a tax rate of only 5% (before - 15%).

- All new small start-up businesses will be exempt from paying the CIT for 1 year.

More information in Lithuanian can be found here.